Predicting Excess Bond Returns using Neural Networks

Project by Polygence alum Anjali

Project's result

Paper in the works + a Machine Learning Model

They started it from zero. Are you ready to level up with us?

Summary

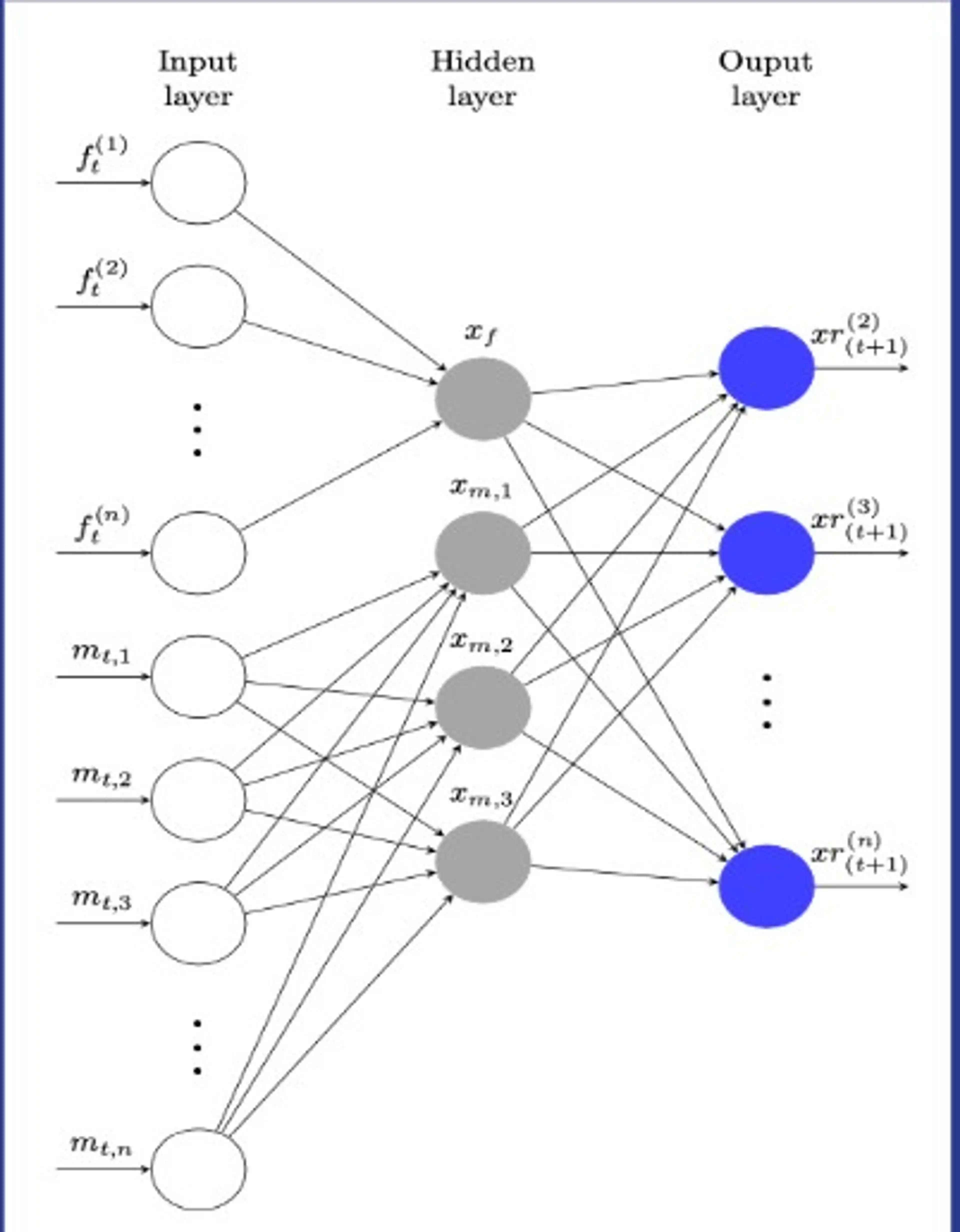

Recent research in financial economics has provided empirical data that suggests that excess returns of Government Bonds can be forecasted using a combination of forward rates and macro-economic factors. A forward rate is the theoretical yield on a bond that is expected to happen in the future. It is calculated by comparing the future expected yield of two bonds. To calculate the forward rate, one uses zero coupon bonds with different maturities. Bond excess returns are positive if the returns on long-term bonds exceed the returns on short-term bonds over this period and negative if the returns on long-term bonds are below the returns on short-term bonds.

Arpit

Polygence mentor

MS Master of Science

Subjects

Computer Science

Expertise

AI/ML, Programming, Career Guidance, Computer Science, Software Eng, AppDev

Check out their profile

Anjali

Student

Hello! My name is Anjali and my Polygence project is about using Neural Networks to Predict Excess Bond Returns!

Graduation Year

2026

Project review

“I enjoyed creating my model and learning how to apply ML to another field. This project started from just an idea and blossomed into an amazing project that has exceeded my expectations in every way. I am truly proud of my work and I hope to share it!”

About my mentor

“It was great to work with Arpit. He was very knowledgeable and insightful.”

Check out their profile